The Corporate Jet Investor (CJI) Conference in Miami has just concluded, and the private aviation industry remains ‘positive’ in its outlook.

The Conference sees aircraft company CEOs, jet-card executives, aviation attorneys, aircraft brokers, and private equity reps coming together for 3 days of interviews and panel discussions. They agreed that the market remains strong following the unprecedented highs of the COVID pandemic; the fractional and jet-card segments are still above pre-Covid sales levels, while others such as used aircraft sales and on-demand charter have declined from giddy highs in 2021 and 2022.

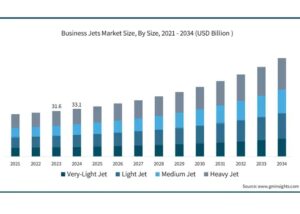

According to WingX, The global private jet market is projected to reach $39.84 billion in 2025 from an estimated $25.87 billion in 2021.

There is no doubt that the United States dominates the private jet industry, accounting for 75% of private jet ownership and a market share of over 42.5% in the global business jet market. We wrote an article recently about how the Trump presidency could influence the global private jet industry, and his re-election is already having a beneficial impact. Rollie Vincent, director of JetNet IQ commented: “Our market indicators have gone up 35 points since the election. There are a lot of signs right now that things aren’t going to slow down, at least not for the short term—barring a black-swan event.”

“It’s nuts. We saw our spring being extended beyond its usual season and then summer was really busy,” says Alan Walsh, senior vice president of client management and operations for Sentient, a jet-card maker. He explains that the company expects to sell $100 million worth of flights by the end of the year, and expects a strong year next year, “barring any unforeseen larger issues.”

Fractional Ownership

Sentient’s sister company, Flexjet, has seen its fractional business grow during the Covid years and beyond. The company reported an 11 percent year-to-date sales growth compared to last year, with a waiting list.

For the entire fractional segment, including fractional’s largest firm, NetJets, Flexjet, and nearly a dozen smaller companies, the number of flights was up 59 percent in the second quarter of 2024, compared to the same quarter of pre-covid 2019. A mix of whole aircraft owners, now selling their jets and moving into fractional, charter users, and corporate flight departments are driving the increase.

“Surprisingly, our fractional customer profile has gotten about 10 years younger,” said Kenn Ricci, the principal of Directional Aviation Capital, during the keynote address. “That’s a good thing because they’ll be with us longer. We’re also selling shares in four times as many mid- and super-mid aircraft than we do light jets. So, the jets are getting bigger. The other big change is our international growth.”

Used Aircraft Sales

The used-aircraft market, which softened after frenzied sales activity in 2021 and 2022, seems to be stabilising in the second half of this year, according to Vincent. “Values are holding up higher and longer than we expected, and we expect values to increase in the fourth quarter of this year,” he said. Because of U.S. tax, the fourth quarter sees a surge of business jet sales.

New Aircraft Sales

New business jet deliveries were valued at about $700 million this year, said Vincent, noting there is also a backlog of unbuilt, ordered aircraft valued at about $51 billion. “It’s enough for several years of production,” he said. “That leaves the aircraft manufacturers in good shape.”

On-demand Charter

On-demand charter is the only segment of the market that is softer, according to industry analyst ARGUS, which reported a 5.2 percent drop in total hours during the first half of 2024, compared to the first half of 2023. But the 14.7 percent decline from the 2022 high is even a better indicator in the decline of on-demand charter.

Challenges Ahead

The shortage of aircraft repair technicians, and not enough Maintenance, Repair, and Overhaul (MRO) centres, along with a continued supply-chain shortage of parts, is keeping many aircraft grounded for days, or even weeks. Ricci says a third of the Flexjet fleet is undergoing repairs at any given point. Most experts expect it to continue for several years.

The conference also had panels focusing on new connectivity technologies for aircraft cabins, the use of AI toward pilot-less aircraft, and the FlyHouse app that promises a seamless, Uber-like experience for people who want to book on-demand charters. Jack Lambert, FlyHouse’s founder, said the app lets potential charterers initiate a “reverse auction” among multiple charter firms and gain the best price. “On the low end, we expect this to be a $3 to $5 billion market in five years,” he said.

Surveys

Two surveys show similar long-term outlooks for the business jet market, though one is less rosy about short-term conditions. JETNET iQ’s third-quarter survey and Honeywell’s 33rd Global Business Aviation Outlook.

The Honeywell report forecasts new business jet deliveries in 2025 to be 12 percent higher than 2024, with 90 percent of those surveyed expecting to fly more or about the same in 2025 than this year. Large jets are also expected to account for about two-thirds of all expenditures of new business jets in the next five years.

But JETNET iQ founder Rollie Vincent reported a cloud of “uncertainty” among business aviation buyers and sellers these days, according to the most recent survey. “That was the No. 1 word reported by respondents,” he said during a press conference at BACE.

Optimism regarding current market conditions has been declining since late 2022. The JETNET survey for the third quarter of 2024 reported that global confidence in the market was down 26.4 percent for the third quarter compared to being up 16.8 percent for the same period a year ago.

When respondents were asked about the top industry challenges, the three most pressing included aerospace supply chain recovery, aircraft maintenance repair and overhaul capacity, and attracting and retaining talent to the industry.

In 2021 to 2022, the industry went through a dramatic rebalancing following the COVID pandemic, said Vincent, and it is still healing from disruptions to product and service supply chains.

According to the JETNET survey, aircraft deliveries have been flat worldwide, but backlogs have also been valued at $50 billion yearly since 2022, signifying that “we are not in a demand-weakened world,” said Vincent.

While the U.S. has the most extensive business jet fleet in the world and a healthy, growing annual GDP forecast of 2.4 percent, other countries are experiencing faster growth, including India, China, Venezuela, and United Arab Emirates. “What these countries don’t have are airplanes,” Vincent says, noting an unmet opportunity for business aviation.

Since 2022, very-light to mid-size jet segments showed the most significant increase in pre-owned sale inventories. The JETNET survey also shows that in 2023 the five major airframers were taking more orders than they delivered, which builds a healthy backlog.

Of the 8,600 jets forecasted to be built over the next 10 years, JETNET says light jets (22.6 percent), large ultra long-range jets (22.2 percent), and personal jets (15.4 percent) ranked as the top three segments. Those were followed by super-midsize jets (14 percent), midsize jets (7.3 percent), very light jets (6.1%), large long-range jets (5.1 percent), large jets (5.2 percent), and super-light jets (1.6 percent). Total value will be about $262 billion. JETNET also forecasts the delivery of 4,300 new turboprops through 2033 with a value of $25 billion.

The Honeywell survey noted that the introduction of new aircraft models continues to drive increased demand, a trend that will continue into the early 2030s. The survey said North America will see 66 percent of new jet deliveries over the next five years, which is consistent with historical demand. Europe will have 13 percent of new deliveries during the same time period, and Latin America will account for 10 percent of the deliveries. In the meantime, the Asia Pacific region and Middle East will account for 7 and 3 percent, respectively.

Both surveys reported a cooling for pre-owned aircraft after record-low inventory levels in 2021 and 2022, though Honeywell says aircraft values remain strong compared to the previous decade. “While pre-owned inventory will likely continue to increase slowly, prices should remain stable,” the company said in a statement.

The JETNET study showed that owners who want to sell pre-owned aircraft was much higher than last year, and those who intend to purchase these aircraft, while lower than the number of sellers, has risen this year, perhaps signifying a glimpse of returning stability to the market.

Other macro trends include retooling business aircraft for the next generation of technologies and customer requirements, and a global march to sustainability, which is being led by European countries. “European operators show the most proactive behaviour in lowering their carbon footprint, with North American operators lagging slightly behind,” said the Honeywell report. “However, the total number of operators taking proactive steps in North America is still greater than any other region given the much larger volume of business aviation operations in the region.”

The acquisition of new, fuel-efficient aircraft is considered the most effective way to lower business aviation’s environmental impact, according to the Honeywell survey, though only 60 percent of respondents are “proactively” taking steps to reduce their environmental impact. The use of sustainable aviation fuel is also another method for lowering carbon emissions, though 75 percent of operators say its higher cost is an obstacle to implementation.